Decentralised finance (DeFi) has emerged as a fast-growing section throughout the cryptoasset ecosystem. DeFi is an umbrella time period generally used to explain quite a lot of providers in cryptoasset markets that goal to duplicate some capabilities of the standard monetary (TradFi) system, purportedly by disintermediating their provision and decentralising their governance. In DeFi, the function of monetary establishments and market infrastructures is changed to various levels by self-executing code, or so-called sensible contracts.1

The turmoil in cryptoasset markets and in DeFi in 2022 uncovered quite a few vulnerabilities in relation to DeFi, together with operational fragilities and liquidity and maturity mismatches, in addition to points regarding leverage and interconnectedness. Up to now, these vulnerabilities haven’t affected the standard monetary system as a consequence of DeFi’s comparatively small dimension and restricted interconnectedness with conventional markets. Nevertheless, the size of DeFi and/or its hyperlinks with TradFi could develop over time, elevating the potential for contagion and threats to monetary stability.

Towards this background, the Monetary Stability Board (FSB) printed a report in 2023 entitled The Monetary Stability Dangers of Decentralised Finance to offer an summary of the principle options and vulnerabilities of DeFi, assess potential monetary stability threats and draw coverage implications.

Background of DeFi

DeFi providers are in-built a multi-layered structure that features permissionless blockchains,2 sensible contracts, DeFi protocols3 and purportedly decentralised functions (DApps). DApps can replicate some capabilities of the standard monetary system. These embrace decentralised exchanges (DEXs), decentralised types of lending, derivatives issued and traded in a decentralised system, preliminary types of decentralised insurance coverage and asset administration.

The DeFi ecosystem is a posh internet of interconnections involving a number of gamers with various interrelationships and pursuits. They embrace protocol creators and builders, so-called decentralised autonomous organisations (DAOs),4 funders (eg enterprise capital and personal fairness funds) and institutional and retail finish customers, amongst others. DApps purport to have decentralised possession and governance buildings if they’ve such buildings in any respect. Nevertheless, in some DeFi functions, decision-making is centralised and, in sensible phrases, the precise diploma of decentralisation amongst underlying DeFi organisational buildings varies broadly.

The DeFi market is pushed largely by institutional contributors in superior economies. In distinction, there may be comparatively little direct participation from retail buyers and rising or low-income economies. Up to now, DeFi is especially self-referential, within the sense that DeFi services and products work together primarily with different DeFi services and products moderately than with TradFi and the actual financial system.

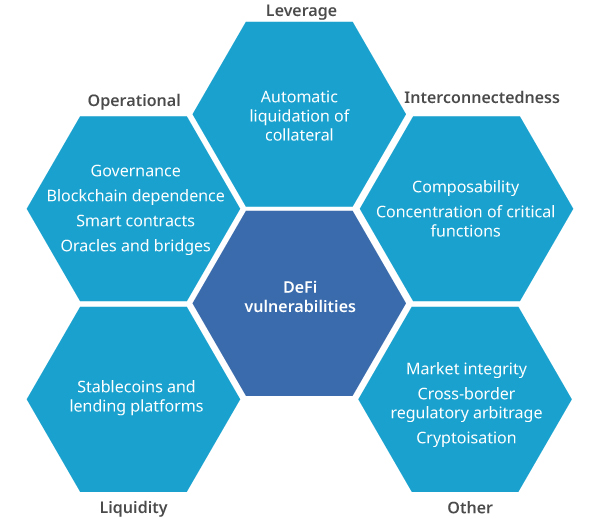

DeFi vulnerabilities, interlinkages and transmission channels

Whereas the processes to offer providers are in lots of circumstances novel, DeFi doesn’t differ considerably from TradFi within the capabilities it performs. In making an attempt to duplicate a few of the capabilities of the TradFi system, DeFi inherits and should amplify the vulnerabilities of that system. This consists of well-known vulnerabilities regarding operational fragilities, liquidity and maturity mismatches, leverage and interconnectedness.

Nevertheless, DeFi’s particular options could end in these vulnerabilities typically enjoying out in a different way than in TradFi, for instance on account of spillover results associated to the automated liquidation of collateral based mostly on sensible contracts or dependence on the underlying blockchain. The amplification of identified vulnerabilities comes from novel technological options, the excessive diploma of structural interlinkages amongst the contributors in DeFi and from non-compliance with current regulatory necessities or lack of regulation.

The extent to which DeFi vulnerabilities can result in monetary stability considerations largely relies on the interlinkages and related transmission channels between DeFi, TradFi and the actual financial system. These channels embrace monetary establishments’ exposures to DeFi; confidence and wealth results stemming from the involvement of households and corporations in DeFi; and the extent to which DeFi functions could facilitate the usage of cryptoassets for funds and settlement. Up to now, these interlinkages are restricted, as proven by the modest impression of the 2022 cryptoasset market turmoil on TradFi.

Conclusions

In future, one believable situation is that DeFi continues to develop and turns into extra interconnected with the actual financial system and the broader monetary system. Thus, the FSB report highlights the necessity to rigorously monitor vulnerabilities inherent in DeFi and potential threats to monetary stability which is hampered by the absence or low high quality of obtainable information, the dearth of or non-compliance with reporting necessities, and market practices oriented in direction of working in opaque and non-transparent methods.

Within the mild of those findings, the FSB report places ahead a number of issues for future work. First, the FSB will proactively analyse the monetary vulnerabilities of the DeFi ecosystem as a part of its common monitoring of the broader cryptoasset markets. Second, the FSB, in collaboration with regulatory authorities and different standard-setting our bodies, will discover approaches to measure and monitor DeFi interconnectedness with TradFi. Third, as each the use circumstances and regulatory approaches round DeFi are nonetheless evolving, the FSB will discover the extent to which its proposed coverage suggestions for the worldwide regulation of cryptoasset actions could must be enhanced to take account of DeFi-specific dangers and facilitate the enforcement of guidelines.

- A sensible contract is a cryptoasset time period that refers to self-executing functions that may set off an motion if some pre-specified situations are met.

- A blockchain is a type of distributed ledger through which particulars of transactions are held within the ledger within the type of blocks of knowledge. A block of latest info is connected into the chain of pre-existing blocks through a computerised course of by which transactions are validated. A permissionless blockchain permits anybody to entry the community and take part within the validation of transactions, whereas a permissioned one permits solely a pre-selected group of contributors to entry the community and validate transactions.

- A DeFi protocol is a specialised system of guidelines that creates a program designed to carry out conventional monetary capabilities.

- A DAO is, in concept, a decentralised software consisting of guidelines of operation that dictate who can execute a sure motion or make an improve. Code helps create an organisational construction supposed to operate with out a centralised administration construction.

This Government Abstract and associated tutorials are additionally out there in FSI Connect, the web studying instrument of the Financial institution for Worldwide Settlements.

Supply: BIS

NEWSLETTER SIGN UP

And obtain unique articles on securities markets

{kind=link}