The way in which bitcoin choices are priced exhibits that merchants are paring their bullish bias because the U.S. Securities and Alternate Fee’s (SEC) Jan. 10 deadline to approve spot exchange-traded funds nears.

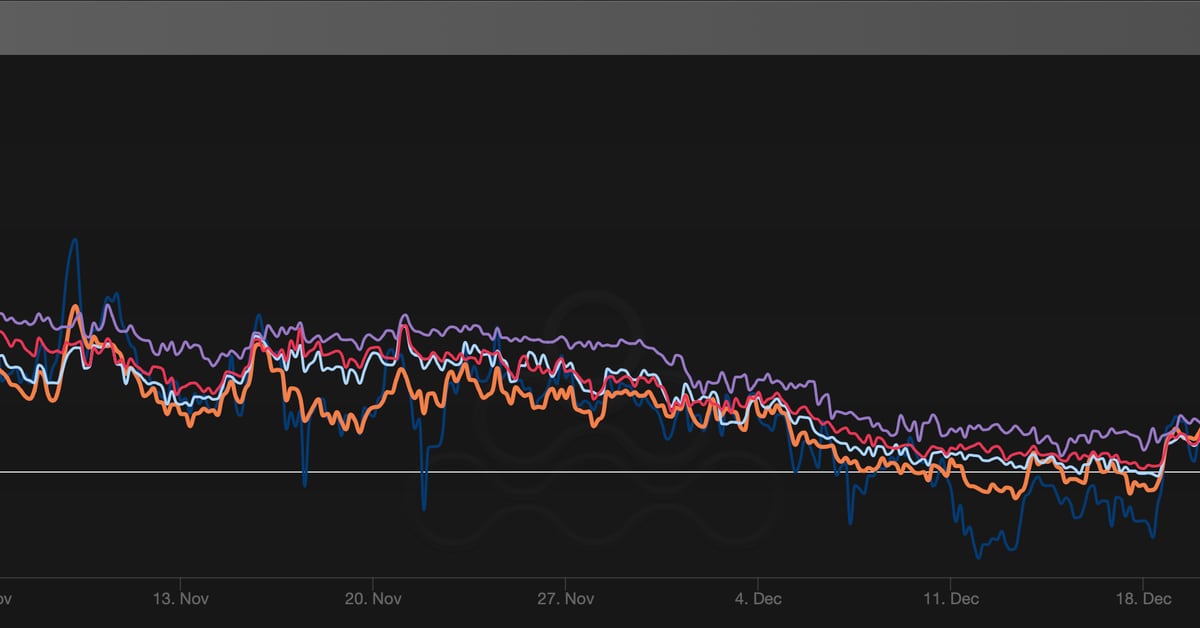

Choices skew tracked by Amberdata present calls expiring in a single week, one, two, and three months buying and selling at a premium of round 2% to places versus 8% in early November. The regular retreat is reflective of extra measured bullish sentiment towards bitcoin.

Calls give the customer the best however not the duty to buy the underlying asset at a predetermined value at a later date. A name purchaser is implicitly bullish in the marketplace, whereas a put purchaser is bearish. Choices skew gauges relative demand for calls versus places.

Maybe merchants are in a wait-and-watch mode forward of the anticipated ETF resolution. Per some analysts, the cryptocurrency, having surged by 61% in three months on the again of ETF expectations, is likely to drop as soon as the extremely anticipated choices go stay.

The weakening of name bias in longer period skews can also be consistent with the out-of-consensus evaluation that claims billions of {dollars} in inflows into ETFs will possible occur over time somewhat than instantly.

The one-week choices ATM implied volatility, which exhibits the market’s expectations for value turbulence over the subsequent seven days, have virtually doubled to an annualized since Dec. 29, surpassing longer period gauges.

It is a warning for merchants to remain alert within the lead-up to and instantly after the Jan. 10 deadline.

Longer period implied volatility gauges have seen extra minor upticks; an indication merchants count on ETF bulletins to have a fleeting affect on the diploma of value volatility. Furthermore, some analysts count on ETFs to weigh over value turbulence in the long term.

{kind=link}