Key Takeaways

- In 2023, the OECD launched a brand new framework for crypto asset tax reporting.

- As nations world wide implement the brand new requirements, crypto companies’ tax reporting burden is ready to extend.

- This creates a problem for brokers and different intermediaries which must gather and manage big volumes of knowledge.

In 2023, the Group for Financial Cooperation and Improvement (OECD) launched a brand new framework for crypto asset tax reporting designed to allow higher information-sharing between nations. As nationwide authorities act to implement the brand new requirements by 2027, crypto brokers world wide have discovered that their reporting obligations are growing.

Based on PwC’s 2024 Crypto Tax Report , the OECD tips may incur billions of {dollars} of further prices yearly as tax reporting necessities develop to a higher vary of transactions.

OECD Crypto Tax Guidelines

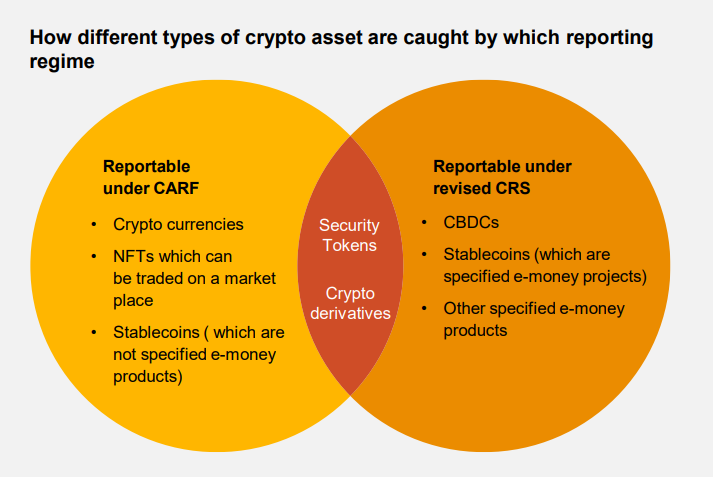

The OECD’s crypto asset reporting framework (CARF ) requires exchanges, brokers, custodians and pockets suppliers to gather and report back to native tax authorities data regarding the identification and transactions of their customers.

The framework covers cryptocurrencies, tokenized real-world assets, stablecoins and a few NFTs. Reportable transactions embrace crypto-for-crypto swaps, fiat on- and off-ramps, and transactions the place crypto is used to pay for items or providers valued at greater than $50,000.

Jurisdictions which have already moved to implement the brand new guidelines embrace the US, the place the Treasury proposed rules final August, and the EU, the place the council adopted a directive amending the bloc’s tax code in October.

In each instances, the brand new reporting necessities are anticipated to come back into drive by the 2025/2026 tax yr.

Crypto Corporations Brace for Elevated Reporting Burden

With crypto companies reporting burden set to extend considerably, the PwC report notes that

“the quantity of knowledge that can must be gathered, organized and reported can solely be managed through new know-how options.”

Given the digital and sometimes on-chain nature of a lot of the data that must be reported, there are vital alternatives for automation.

For each particular person and company taxpayers, platforms like Coinledger and Bitwave promise to optimize the method of crypto tax administration by integrating with totally different wallets to assist calculate tax payments.

Nevertheless, issues get much more sophisticated relating to worldwide transactions.

Cross-Border Complexity

Though the CARF framework is meant to make it simpler to share data throughout borders, it might probably’t erase the friction between tax regimes.

Take into account, for instance, 2 neighboring nations which have very totally different tax programs: France and Belgium.

In France, traders should pay capital beneficial properties tax on any revenue they make promoting crypto. Then again, Belgium doesn’t distinguish between capital beneficial properties and earnings, taxing every particular person’s earnings from employment or investments collectively.

Historically, capital beneficial properties tax is paid within the nation the place a sale happens whereas earnings tax is paid in your nation of residence.

So what about somebody who resides in Belgium however sells crypto by way of a French change? In principle, they need to be capable to pay capital beneficial properties tax in France after which deduct that from their Belgian legal responsibility to keep away from double taxation. However this requires advanced reporting in each jurisdictions.

The Crypto Tax Hole

Cryptocurrencies like Bitcoin are borderless by nature. However exchanges, brokers and different intermediaries aren’t, and when the final word liquid asset meets inflexible tax regimes, it typically slips by way of the gaps.

Calculating the crypto tax gap is tough, however by most accounts, evasion is pretty commonplace

Take into account, for instance, that though only one% of 2020 US tax returns declared cryptocurrency gross sales, but surveys recommend that between 10% and 20% of the inhabitants personal digital belongings.

This discrepancy is without doubt one of the major motivations for the OECD’s new reporting tips, which is able to assist tax authorities hold higher observe of who owns what.

Within the fashionable world of Bitcoin ETFs and institutional crypto adoption, off-the-books transactions and informal underreporting will seemingly change into much less prevalent, at the very least as a proportion of the general market.

In any case, from the attitude of tax revenues, giant establishments and big crypto funds are far more essential than retail traders dipping their toes in DeFi.

Was this Article useful?

{kind=link}